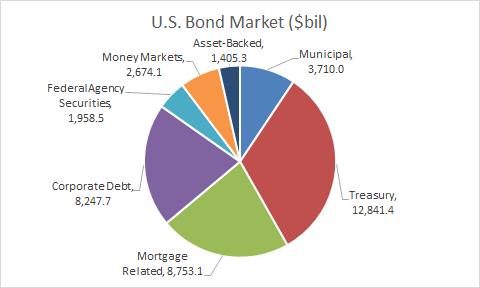

The entire U.S. fixed income market (municipals, Treasuries, mortgages, corporates, federal agency bonds, money market, and asset back securities) totals $39.6 trillion.1

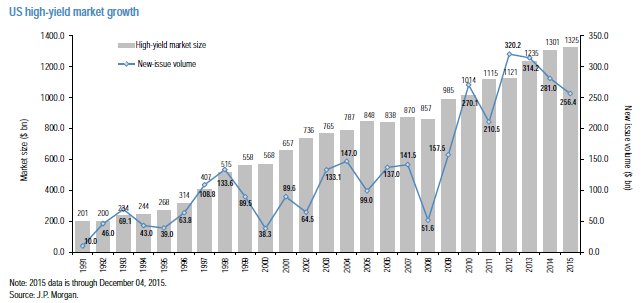

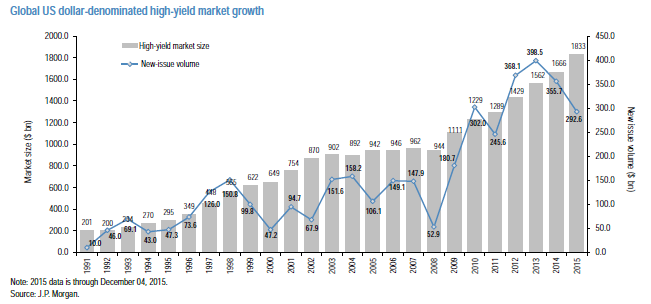

Corporate credit is about $8.2 trillion of this pie. The high yield bond market is a growing piece of that corporate debt piece, now at $1.325 trillion domestically and $1.8 trillion including all US dollar denominated bonds.2

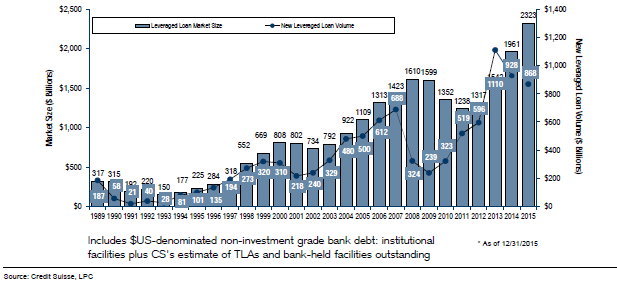

If you add in high yield floating rate loans, that includes another $2.3 trillion and together high yield bonds and loans account for over 30% of corporate debt.3

Leveraged Loan Market Size: Institutional, TLAs and Bank-held Facilities

One thing is clear, that the high yield debt market is a growing market, and one that cannot be ignored for fixed income investors.

However, more recently much has been made of high yield exchange traded funds (ETFs), with some critics speculating that some wider-spread selling in high yield ETFs could cause a collapse in high yield markets due to “liquidity” issues. We have previously explained how recent regulations post the financial crisis have led to less market making and lower dealer inventory of bonds, and the impact that has had on markets (see our piece “Understanding Market Liquidity”). However, it is important to keep in mind the size of the high yield ETF market relative to the entire high yield market.

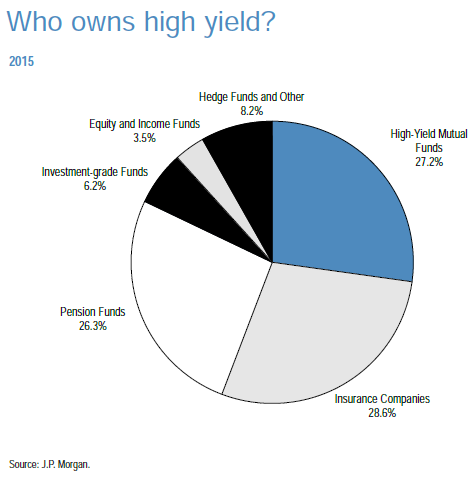

The three largest categories of owners of high yield bonds are pension funds, insurance companies, and retail mutual funds, all of which have relatively similar size of ownership at just over a quarter of the market each.4

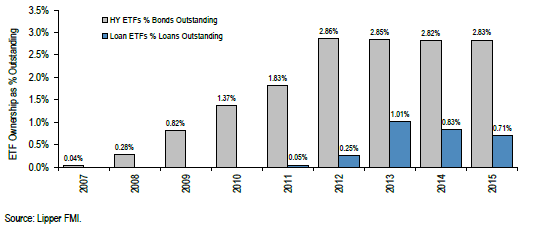

With this we see both institutional and retail customers as active in the space. High yield ETFs account for about 13.5% of the total $271 billion “retail” high yield fund base5, which includes the much larger mutual fund counterpart, and ETFs account for about 2.8% of the broader high yield market and have been around the level for the last four years.6

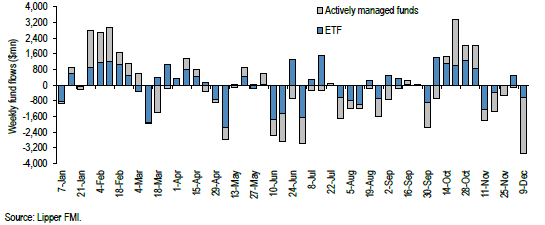

Flows in and out of these “retail” mutual and exchange traded funds (though we know that various institutions are buyers of mutual and ETFs as well) can be volatile week over week, but again, these flows pale in comparison to size of the total market.7

Weekly mutual fund and ETF inflows

For instance looking back over 2015, the largest weekly reported exchange traded and mutual fund flows totaled around $3.8 billion, which compared to a $1.8 trillion market means it is about 0.2% of the total market, so very small. Across the high yield market, in funds and beyond, we are seeing selling pressure, which in this environment of lower dealer inventory is leading to heightened price volatility. While on the fund side, again, these weekly flows are a very small portion of the entire market, though as we have pointed out before, we believe that high yield ETFs provide an advantage over mutual funds during volatile times because ETFs trade/price intra-day, so we would argue provide a more accurate and true pricing mechanism for going in and out of the high yield market than mutual funds that only trade at the end of the day.

Turing back to the total corporate debt market, again, high yield bonds are a $1.8trillion market just domestically, while loans are $2.3trillion. A lot has been made in the media of high yield’s exposure to energy. Yes, it is definitely something high yield investors need to be cognizant of, especially in index based products. Energy accounts for 14.6% of the index, with metals and mining another 5.1%.8 However, this leaves 80% of the $1.8trillion market not directly related to these problem industries. At today’s prices and yields, we believe there are plenty of attractive opportunities for value-based, active investors.

We believe that high yield ETFs provide investors great accessibility the asset class. And while the recent regulations may add an element of volatility to the market, we would view this volatility as an opportunity for active managers who can capitalize on discounts and can be intentional about the credits they invest in. There is much to avoid in this large and growing market, but we believe there is even more to embrace for actively managed products that can pick and choose what securities they believe will outperform in the environment ahead.